Compare

business loans

personal loans

property loans

from 25+ reputable banks in Singapore

Approved Consultancy’s complimentary in-house assessment will not affect your credit score and you will receive a tailored list of options based on your eligibility from different major banks or funding institutions.

Our complimentary assessment will not affect your credit score

Compare

business loans

personal loans

property loans

from 25+ reputable banks in Singapore

Our complimentary assessment will not affect your credit score and you will receive a tailored list of options based on your eligibility from different major banks or funding institutions.

Our complimentary assessment will not affect your credit score

Borrow from

1 month to 30 years

Get a loan proposal

with no commitment

Find the lowest interest rates now!

How do we actually

benefit you?

-

Lower Interest Costs

Imagine wanting to buy an Iphone but having someone you know who works at Apple saves you 15%, save more when you use our extensive network of bankers. -

Fast and Convenient Comparison

Skip the hassle of contacting multiple banks one by one. Compare over 25+ lenders easily through our platform and get results faster. -

Completely Risk-Free Process

Our assessment tool is 100% free to use — no login, no Singpass, and no up front fees. -

Rejected? We Can Still Help

Even if your loan application was turned down, our trusted partner network of lenders may still have options for you. Get a second chance to secure the financing you need.

-

Lower Interest Costs

Imagine wanting to buy an Iphone but having someone you know who works at Apple saves you 15%, save more on interest rates when you use our extensive network of bankers. -

Fast and Convenient Comparison

Skip the hassle of contacting multiple banks one by one. Compare over 25+ lenders easily through our platform and get results faster. -

Completely Risk-Free Process

Our assessment tool is 100% free to use — no login, no Singpass, and no up front fees. -

Rejected? We Can Still Help

Even if your loan application was turned down, our trusted partner network of lenders may still have options for you. Get a second chance to secure the financing you need.

How does the

free assesment work?

Contact us a few quick details about your loan needs — no lengthy forms or paperwork required. Our team will review your profile instantly.

We’ll assess your eligibility and connect you directly with lenders that best fit your goals — saving you hours of searching and rejections.

We’ll show you the top options side by side, so you can pick the deal that saves you the most. No hidden fees, no pressure — just easy financing.

Loan calculator

Our business loan interest rates start at 1.5% a month.

We’ll only charge interest on your outstanding balance for the days you’re using your business loan.

Borrowing for over 12 months may incur an additional fee, typically it’s 5% when borrowing for 13 to 24 months and 6% for longer.

This loan calculator is only an example, your actual rate and repayment amount for your business loan will vary based on your circumstances.

What do you need

to get started?

We can accept applications from all individuals and businesses (no matter the age or industry), in fact all we ask is:

- You're an individual based in Singapore

- For businesses, minimum 30% local shareholding

What you need to have to hand:

- Credit Bureau Report

- 2024 & 2025 Notice Of Assesment (NOA)

Ready to apply?

The document requirements may change according to the loan size and type of company

What do you need to get started?

We can accept applications from all individuals and businesses (no matter the age or industry), in fact all we ask is:

- You are an individual based in Singapore

- For businesses, minimum 30% local shareholding

What you need to have to hand:

- Credit Bureau Report

- 2024 & 2025 Notice Of Assesment (NOA)

Ready to apply?

The document requirements may change according to the loan size and type of company

Get fast, flexible funding on your terms

How does it work?

- Submit the contact form with the relevant details

- Our team will contact you to start the assessment

- Receive your very own tailored loan proposal suited for your needs

Still need help?

- Find answers in our FAQ

- admin@approvedconsultancy.com

Loan Proposal Form

Frequently asked questions

Here are some questions our customers ask. Check our FAQs for anything we haven’t covered.

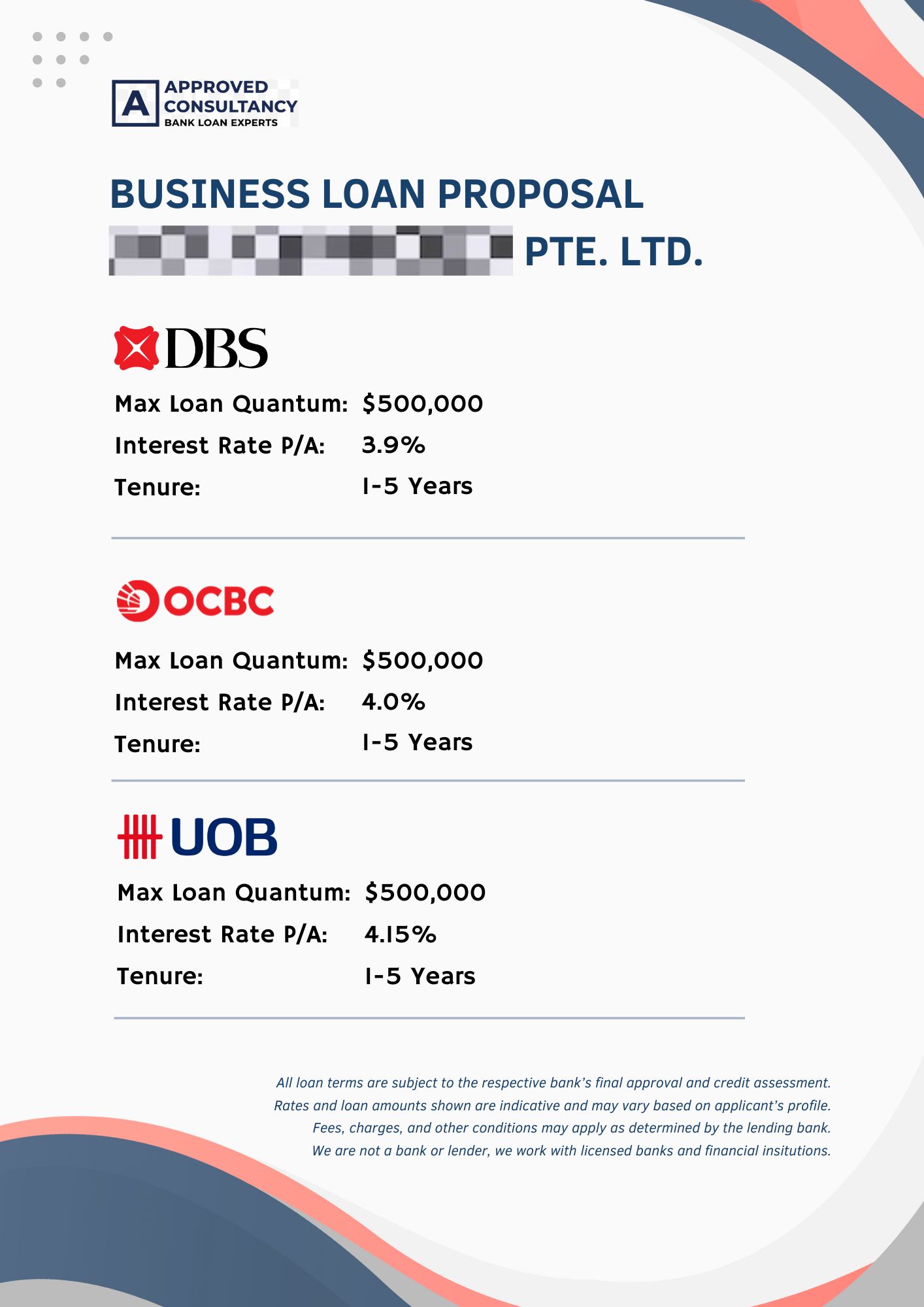

The maximum business-loan amount in Singapore varies significantly depending on your business’s financial position (such as revenue, industry, cash-flow) and the lender’s criteria. For many small to medium enterprises (SME), bank-term loans tend to offer up to S$500,000 is all criterias are met.

Under government-assisted schemes:

The Enterprise Financing Scheme – SME Working Capital Loan (EFS-WCL) offers up to S$500,000 per borrower for eligible SMEs.

The Enterprise Financing Scheme – Trade Loan (EFS-TL) allows up to S$10 million per borrower for trade-financing purposes.

A typical business-loan application in Singapore may proceed as follows:

Many lenders report approval times from submission of complete documents to decision in about 5 to 15 business days.

From application to actual disbursement of funds may take roughly 3 to 5 weeks, accounting for document preparation, internal reviews, bank approval and funds transfer.

Timeliness depends heavily on how complete and clear your documents are, how well you meet the lender’s criteria, and whether additional information or clarifications are needed.

In Singapore, there are nearly 20 major banks and over 20 financial institutions offering business loans to SMEs. There isn’t a single “best” bank — it really depends on your company’s profile and the bank’s lending criteria. Each bank has its own credit requirements and risk appetite.

Some may prefer certain industries, while others may avoid them altogether. Because of this, businesses often spend a lot of time approaching banks that may not be the right fit.

Beyond the major banks, there are also alternative financiers providing flexible financing solutions tailored for SMEs. With our experience and network, we can help match your business to the most suitable lenders — improving your chances of approval and helping you secure the best possible terms.

Business loan applications can be declined for several reasons, including:

Applying to banks that don’t match your business profile

The owner’s personal credit history

Existing loan limits with your current bank

Weak or inconsistent cash flow

Imagine needing funds quickly to secure a project or tender — only to have your loan rejected. This could delay or even derail your business plans.

What’s more, once a bank rejects your application, you may need to wait 6 to 12 months before reapplying with the same bank.

That’s why it’s important to approach the right lenders and prepare your application properly to avoid rejection.

There are several types of business-financing products suitable for different needs. For instance:

Working-capital or term-loans: for general operational funding, expansion, cash-flow support.

Trade-financing: for inventory purchases, export/import, supplier payments.

Asset-financing: for equipment, machinery, property.

Invoice factoring- or receivables-financing: converting unpaid invoices into liquidity.

Choosing the “right” type means matching the facility to your purpose, repayment capacity and risk profile. When you contact us, we will clarify which option aligns best with your business goals.

Your borrowing limit depends on your monthly income, credit rating, and the bank’s assessment.

Most banks in Singapore allow qualified borrowers to take up to 4 to 6 times their monthly income.

If your income is above S$120,000, individuals can borrow up to 8 to 12 times their monthly income

However, if your annual income is below S$20,000, the amount you can access may be lower or available only through select financial institutions.

Every bank applies its own formula — so the loan amount can vary widely between lenders.

If you’re unsure how much you qualify for, a quick in-house assessment check through us can help you understand your borrowing range instantly and identify which lenders are most likely to approve your application.

Interest rates generally range between 1.58% and 7% per annum, depending on your credit standing, income level, and chosen tenure.

Once fees and charges are included, the Effective Interest Rate (EIR) usually falls between 2.9% and 14% per annum.

Because rates differ across banks and change regularly, it’s best to compare offers from several lenders rather than applying with just one.

A well-structured comparison provided by us can often reduce your total interest cost significantly over the loan term.

When all required documents are in place, most banks can approve a personal loan within 1 to 3 working days.

If further checks are needed, the process may take up to a week, and funds are typically disbursed directly to your account shortly after approval.

If timing matters — such as when you need to consolidate debts or cover urgent expenses — we will immediately help to ensure your application is complete, accurate, and sent to the right lenders from the start.

This often shortens the approval process and avoids unnecessary re-submissions.

Yes, it’s possible. Banks will review your Total Debt Servicing Ratio (TDSR) to ensure your income can support another loan.

If a new personal loan isn’t feasible due to high existing debt, there are other options:

Debt consolidation plans to merge multiple loans into one manageable repayment, or

Balance-transfer or refinancing solutions that can lower your overall interest costs.

Understanding which approach best fits your financial situation can make a big difference in maintaining a healthy credit record.

Absolutely. Your Credit Bureau Singapore (CBS) score and repayment history play a key role in determining your eligibility, interest rate, and loan amount.

A strong credit score improves your approval odds and gives you access to more competitive rates, while a weaker score may limit your options.

If you’re uncertain about your score, you can easily obtain your credit report from CBS.

We will review it before applying as it helps identify any issues early — and gives you time to make improvements that can strengthen your application.

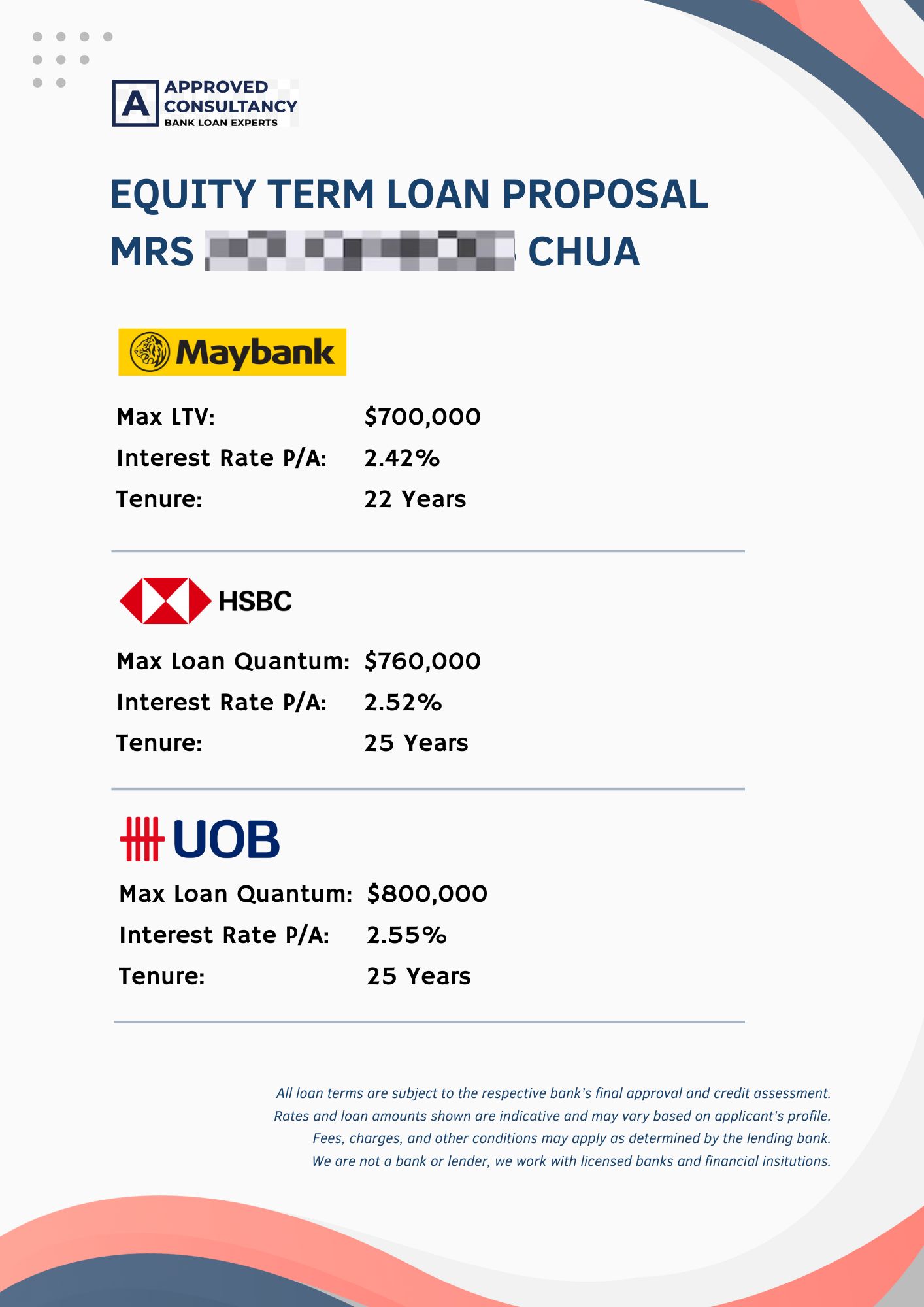

An equity term loan allows property owners to unlock the value of their real estate by borrowing against its equity.

In simple terms, the bank or lender gives you a lump-sum loan secured by your property — usually up to a percentage of its current market value.

You continue to retain ownership of the property while repaying the loan in monthly instalments.

This type of financing is commonly used for business expansion, investment, or cash flow needs, without having to sell the property.

The amount you can borrow depends on your property type, outstanding loan balance, and the lender’s loan-to-value (LTV) ratio.

Most banks in Singapore offer up to 75% of the property’s market valuation (combined with any existing mortgage).

Private funders may offer flexible terms but usually at higher interest rates.

If your property has no existing loan, you can typically access a larger quantum — making it an efficient way to raise capital for personal or business use.

A mortgage loan is used to purchase a property, while an equity term loan is used to borrow against a property you already own.

Both are secured loans, but they serve different purposes:

Mortgage loan → for buying a new property.

Equity term loan → for unlocking cash from an existing property’s value.

Equity loans often have shorter tenures and slightly higher interest rates than standard mortgages, but they provide flexibility to use the funds however you wish.

Eligibility depends on property ownership, loan repayment history, and financial standing.

Generally, applicants must:

Be Singapore Citizens or Permanent Residents (foreigners may apply for selected property types).

Own a fully or partially paid-up private or commercial property in Singapore.

Demonstrate sufficient income and a healthy credit profile to service the loan.

Some lenders also accept corporate borrowers (for business equity term loans) using company-owned properties.

One of the main advantages of an equity term loan is flexibility of use.

Borrowers commonly use the funds for:

Business expansion or investment opportunities

Property renovation or upgrading

Education, medical, or family expenses

Debt consolidation or refinancing of higher-interest loans

Banks generally do not restrict how you use the funds, as long as it complies with local regulations.